- AUD/USD clinched marginal gains in the low-0.6500s on Wednesday.

- The US Dollar remained bid on the back of trade jitters and Trump’s tariffs.

- Markets are focussing on Trump’s threats of additional tariffs.

The Australian Dollar (AUD) added to its recent rebound against the US Dollar (USD) on Wednesday, with AUD/USD revisiting the 0.6550 region amid a humble daily uptick.

RBA holds firm but signals easing bias

The Reserve Bank of Australia’s (RBA) unexpected decision to keep the Official Cash Rate (OCR) unchanged at 3.85% on Tuesday defyed widespread expectations of a 25-basis-points cut.

Indeed, the central bank revealed that its policy decision was split, with six board members voting to hold and three favouring a reduction. Governor Michele Bullock clarified that this divide reflected differences over timing, not direction, and reiterated that the board remained inclined toward an easing path, provided inflation data for the April-June period came in broadly as forecast.

Markets quickly adjusted to the RBA’s tone, assigning nearly a 90% chance of a quarter-point cut at the August 12 meeting and revising the expected terminal rate from 2.85% to 3.10%.

On Wednesday, Deputy Governor Andrew Hauser remarked that Australia’s central bank is highly attentive to developments regarding US tariffs, noting that there exists a significant level of uncertainty in the global economy. Hauser remarked that the impact of the tariff on Australia is still in its early stages, noting that the sentiment among businesses and households has not significantly deteriorated, unlike the sentiment observed in the United States and Europe.

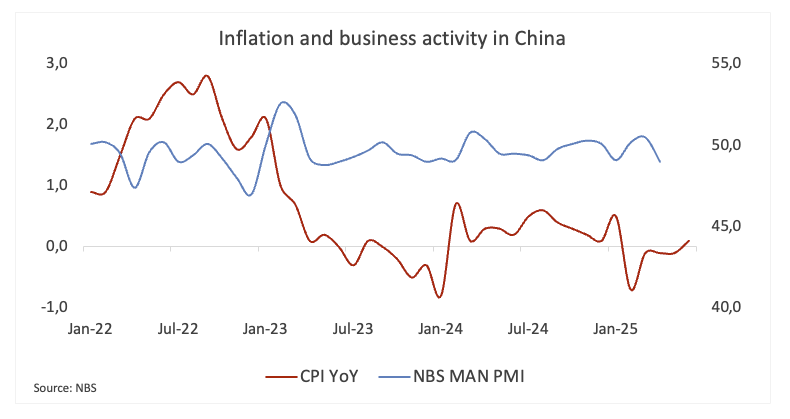

Mixed signals from China

Meanwhile, recent data from China offered a mixed picture. May figures showed improvements in industrial output, retail sales, and services activity, while official PMI readings hovered near the expansion threshold. These developments support projections of around 5% GDP growth this year.

However, potential headwinds for Australia’s commodity-sensitive economy included ongoing weakness in the property sector and a gradual withdrawal of stimulus.

In addition, the disinflationary pressure remained well in place in the country after the Consumer Price Index (CPI) rose marginally by 0.1% in the year to June (from -0.1% YoY).

Coincident central bank views?

The Federal Reserve (Fed) decided to keep rates unchanged in June, while the RBA shocked markets by delivering a cautious hold in spite of a consensus on the trajectory of monetary policy. In the event that inflation makes a significant turnaround, Fed Chair Jerome Powell cautioned that US tariffs might rekindle goods inflation, perhaps leading to a split in central bank outlooks.

Speculative positioning eases

CFTC data through July 1 showed non-commercial net shorts in AUD falling to just over 70K contracts, a two-week low, while open interest climbed for a third consecutive week to around 151.4K contracts, suggesting a modest easing in bearish sentiment.

Technical setup

Resistance is seen at the 2025 ceiling of 0.6590 (June 30), followed by the November 2024 high at 0.6687 (November 7) and the key psychological level of 0.7000.

Initial support sits at the 200-day SMA at 0.6409, ahead of the June trough at 0.6372 (June 23) and the May low at 0.6356 (May 12). A break below that zone could expose the 0.6000 level and the 2025 bottom at 0.5913 (April 9).

Momentum signals are mixed: the Relative Strength Index (RSI) above 53 suggests a potential recovery, while an Average Directional Index (ADX) reading near 18 is indicative that the strength of the trend might be subsiding.

AUD/USD daily chart

Medium-term outlook

In the near term, AUD/USD may remain range-bound unless a major shift emerges in China’s policy stance or US trade dynamics.

With the RBA likely to proceed cautiously and China’s recovery still uneven, the Australian Dollar could struggle to break above key resistance levels in the weeks ahead.

GDP FAQs

A country’s Gross Domestic Product (GDP) measures the rate of growth of its economy over a given period of time, usually a quarter. The most reliable figures are those that compare GDP to the previous quarter e.g Q2 of 2023 vs Q1 of 2023, or to the same period in the previous year, e.g Q2 of 2023 vs Q2 of 2022. Annualized quarterly GDP figures extrapolate the growth rate of the quarter as if it were constant for the rest of the year. These can be misleading, however, if temporary shocks impact growth in one quarter but are unlikely to last all year – such as happened in the first quarter of 2020 at the outbreak of the covid pandemic, when growth plummeted.

A higher GDP result is generally positive for a nation’s currency as it reflects a growing economy, which is more likely to produce goods and services that can be exported, as well as attracting higher foreign investment. By the same token, when GDP falls it is usually negative for the currency. When an economy grows people tend to spend more, which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation with the side effect of attracting more capital inflows from global investors, thus helping the local currency appreciate.

When an economy grows and GDP is rising, people tend to spend more which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold versus placing the money in a cash deposit account. Therefore, a higher GDP growth rate is usually a bearish factor for Gold price.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.