- The Bank of England is expected to keep its policy rate at 4.25%.

- UK inflation figures remain well above the BoE’s target.

- GBP/USD maintains its trade in the upper end of the range near 1.3600.

The Bank of England (BoE) is set to reveal its latest monetary policy decision on Thursday, coinciding with its fourth rate-setting meeting of 2025.

Market analysts anticipate that the central bank will keep its benchmark interest rate steady at 4.25% after the reduction announced during the May 8 meeting.

The Monetary Policy Committee’s (MPC) decision will be followed by the release of Meeting Minutes, which will detail the internal discussions that shaped the outcome.

As the rate decision appears to be largely anticipated, investors are likely to shift their focus to the anticipated performance of the UK economy, which presents mixed signals. Key considerations will include the potential trajectory of interest rates, the ongoing debate over tariffs, and the recent developments surrounding the US-UK trade agreement.

Rates, elevated inflation and tariffs

The Bank of England has reduced its policy rate by a quarter point to 4.25% as of May 8, following a notably divided vote among the Monetary Policy Committee (MPC): Swati Dhingra and Alan Taylor supported a more significant half-point cut, while Chief Economist Huw Pill and Catherine Mann argued for keeping interest rates unchanged.

The “Old Lady” has updated its inflation forecast for the year and is now projecting a peak of around 3.50%. This adjustment signifies a reduction from a prior estimate of 3.75%, while simultaneously reflecting an increase from the latest official figure of 2.60% noted in March. Experts predict that inflation will reach the 2% target by the first quarter of 2027.

The central bank has forecasted a 1% growth rate for the economy this year, an increase from the previous estimate of 0.75%. The revision reflects a robust conclusion to 2024, bolstered by promising official data from early 2025, which reveals a quarterly growth rate of 0.60% for the first quarter.

The report indicates that the growth surge observed in the January-March period seems to be an isolated incident. As a result, the growth forecast for 2026 has been revised downward to 1.25%, a decrease from the previous estimate of 1.5%.

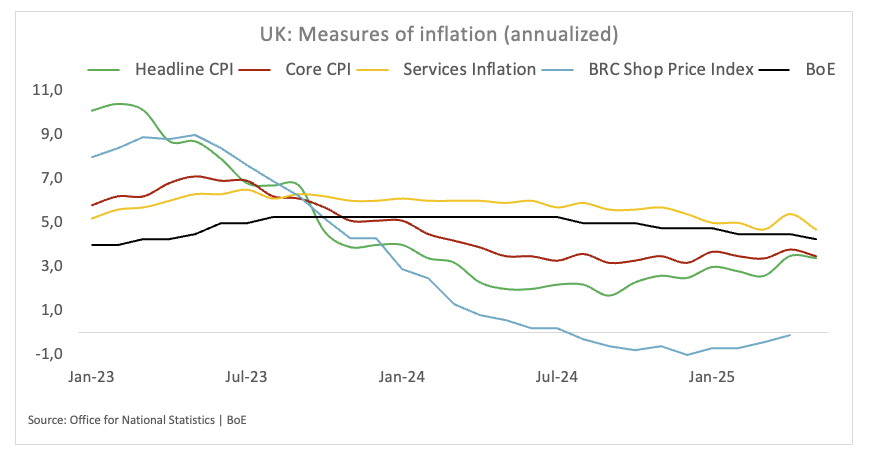

The most recent data released by the Office for National Statistics (ONS) indicates that the annual headline Consumer Price Index (CPI) increased to 3.4% in May. Core inflation, excluding the fluctuating costs of food and energy, increased by 3.50%, indicating a continued trend of easing underlying price pressure. Services inflation, in the meantime, rose by 4.70% over the last 12 months.

In the meantime, some rate setters, Governor Bailey included, showed some caution regarding the easing cycle going forward, as well as the still elevated consumer prices:

Addressing the Treasury Committee, Governor Andrew Bailey said that his approach to reducing interest rates would be “gradual and careful”. He emphasised that these words served as his guiding principles. He stated that, while he continued to anticipate a decline in rates, the trajectory had become “shrouded in a lot more uncertainty” and had turned “unpredictable” due to the turmoil in global trade policy.

Deputy Governor Sarah Breeden informed the committee that she believed a case for a rate cut existed in May, independent of international developments. She assessed that the domestic disinflationary process was advancing as anticipated and was expected to persist.

MPC member Swati Dhingra also noted that she perceives downside risks to the forecast for UK inflation. She said that the recent upticks in inflation are primarily attributed to escalating energy costs rather than fundamental price pressure.

Policymaker Megan Greene argued that although the bank anticipates a decline in the recent inflation surge, it remains “not sanguine” regarding the outlook. She cautioned about the considerable risk posed by potential second-round effects.

How will the BoE interest rate decision impact GBP/USD?

Investors expect the BoE to retain its reference rate at 4.25% on Thursday at 11:00 GMT.

While the result is fully priced in, attention will focus on the vote split among MPC members, which might be a market mover for the British Pound if it indicates an atypical vote.

In the run-up to the meeting, GBP/USD appears to have met decent contention around the 1.3400 zone, driven by US Dollar (USD) dynamics and shifting sentiment toward US trade policy, as well as reignited geopolitical jitters.

“Cable came under some unconvincing downside pressure after hitting more than three-year highs north of 1.3600 the figure on June 13,” said Pablo Piovano, senior analyst at FXStreet. He noted that a decisive break above the yearly tops could potentially trigger a move toward the 2022 high of 1.3748 (January 13).

On the downside, Piovano identified the 55-day Simple Moving Average (SMA) at 1.3329 as an initial provisional support, followed by the May trough at 1.3139 (May 12). Once Cable clears the latter, the more relevant 200-day SMA could return to investors’ radar at 1.2922, just before the April floor of 1.2707 (April 7).

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Economic Indicator

BoE Monetary Policy Report Hearings

The Treasury Committee is appointed by the House of Commons to examine the expenditure, administration and policy of HM Treasury, HM Revenue & Customs, and associated public bodies, including the Bank of England and the Financial Services Authority.

Last release: Tue Jun 03, 2025 09:15

Frequency: Irregular

Actual: –

Consensus: –

Previous: –

Source: Bank of England

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.